Stocks slip on hotter than expected Trump tariffs; USD surged

·

Trump’s latest tariffs range from 20%-40%;

potential Chinese tariffs of 40% and various other sectoral tariffs of 25%-50%

may imply an average 22.5% tariff rate

·

This 22.5% tariff rate is higher than the Fed's

estimates of 15.5% as the base case scenario.

·

Trump may again extend his tariffs deadline to

September-December’25-ahead of the US Festival shopping season.

·

Overall, Fed’s uncertainty may linger, but Fed may

start cutting rates from September’25 by @25 bps.

On Monday, July 7, 2025, all focus of the market

was on Trump’s Truth social on his big & beautiful tariffs announcements.

Trump targeted several countries, including BRICS member South Africa and BRICS

partner countries Malaysia and Kazakhstan, as part of his perceived strategy to

address trade imbalances and assert U.S. economic leverage. These announcements

align with his broader threats against BRICS nations, particularly regarding

their potential de-dollarization efforts. President Donald Trump’s recent

tariff announcements, made via Truth Social on July 7, 2025, target several

countries, including BRICS member South Africa and BRICS partner countries

Malaysia and Kazakhstan, as part of his strategy to address trade imbalances

and assert U.S. economic leverage. These announcements align with his broader

threats against BRICS nations, particularly regarding their potential

de-dollarization efforts.

Status of

Trump tariffs tantrum wef from August 1, 2025 (postponed from earlier deadline

of July 9)

Japan:

·

Minimum rate of 25%

and potentially higher 40% tariffs on alleged transshipments; Japan: Talks have

stalled, with Trump threatening 30–35% tariffs

South

Korea:

·

Minimum rate of 25%

and potentially higher 40% tariffs on alleged transshipments;

·

South Korea: Trade

talks with the US will be a chance to advance both countries’ key industries

through a Renaissance Partnership.

·

South Korea: We will step up trade negotiations

with the US to win mutually beneficial results and clear up uncertainties

caused by tariffs

Vietnam:

·

A deal lowers

tariffs from 46% to 20%, with Vietnam allowing more U.S. goods and reducing

transshipped Chinese goods.

·

Minimum rate of

20% on original Vietnamese goods and 40% on perceived transshipment (Chinese

goods rerouted through Vietnam).

Vietnam’s

Trade Deal with the U.S.

On July 2, 2025, Trump announced via Truth Social a

trade agreement with Vietnam, the second country (after the UK) to secure a

deal following his April 2 “Liberation Day” tariffs. The deal sets a 20% tariff

on Vietnamese exports to the U.S., reduced from a threatened 46%, and a 40%

tariff on transshipped goods (e.g., Chinese products labeled “Made in Vietnam”

to bypass U.S. tariffs). In return, Vietnam grants U.S. goods tariff-free

access to its markets, particularly for large-engine vehicles like SUVs.

The agreement, described as a “framework” by

Vietnamese state media, followed a call between Trump and Vietnam’s General

Secretary To Lam. Vietnam committed to “preferential market access” for U.S.

goods and aims to curb transshipment, addressing U.S. concerns about Chinese

goods rerouted through Vietnam.

Vietnam’s $136.6 billion in U.S. merchandise

exports (2024)- including electronics, apparel, and footwear- accounts for ~30%

of its GDP, making it vulnerable to Trump tariffs. The 20% rate, while lower than

the initial 46%, will still raise costs for U.S. consumers (e.g., an 8% price

hike on a $95 pair of shoes). Vietnam was not included in the July 7 letters,

as its July 2 deal preempted further escalation. However, the 40% transshipment

tariff targets Vietnam’s role as a conduit for Chinese goods, with estimates

suggesting 7–16% of its exports involve transshipment, not the one-third

claimed by Trump advisor Peter Navarro.

Vietnam, a BRICS partner, avoided the additional

10% tariff through its trade deal, unlike South Africa (30%), Malaysia (25%),

and Kazakhstan (25%). The deal aligns with Trump’s push to reduce Chinese

influence in supply chains, as Vietnam’s $123 billion trade surplus with the

U.S. (2024) partly stems from Chinese firms relocating there to skirt U.S.

tariffs. Trump is cautious about Vietnam tariffs as Vietnamese goods are

essential for ordinary Americans; otherwise, they may not afford a pair of

decent office shoes and dresses.

Tariff

Details for South Africa, Malaysia, and Kazakhstan:

·

South Africa (BRICS Member): A 30% tariff on all goods exported to the U.S.

will take effect on August 1, 2025. This rate remains unchanged from the 30%

reciprocal tariff announced on April 2, 2025, before the 90-day pause. South

Africa, a key supplier of platinum (accounting for roughly half of U.S. imports

last year), faces significant economic pressure due to its $8.9 billion trade

surplus with the U.S. in 2024.

·

Malaysia (BRICS Partner): A 25% tariff will be imposed starting August 1,

2025, slightly increased from the 24% rate set in April. Malaysia, a major

exporter of semiconductors ($18 billion to the U.S. last year) and participant

in China’s Belt and Road Initiative, had a $24.9 billion trade surplus with the

U.S. in 2024.

·

Kazakhstan (BRICS Partner): A 25% tariff will apply from August 1, 2025,

reduced from the 27% rate announced in April. Kazakhstan, which exports crude

oil and metal alloys to the U.S., had a smaller $1.3 billion trade surplus in

2024. Its alignment with BRICS and China’s Belt and Road Initiative makes it a

target.

·

Laos and Myanmar (Non-BRICS): Both face a 40% tariff starting August 1, 2025,

reduced from 48% for Laos and 44% for Myanmar. These countries, while not

formal BRICS members, are part of Southeast Asia’s economic sphere and have

ties to China’s regional initiatives. Laos exports optical fibers and clothing,

while Myanmar exports mattresses and bedding, with trade surpluses of $763

million and $577 million, respectively, in 2024.

·

Tunisia will receive a 25% tariff from August 1st

Trump’s letters sent on July 7 indicate failed

talks with these countries, with Trump unilaterally setting rates rather than

securing bilateral deals. White House Press Secretary Karoline Leavitt noted

that Trump would sign an executive order extending the deadline to August 1 for

some countries negotiating in “good faith,” but South Africa, Malaysia, and

Kazakhstan were not granted extensions, as evidenced by the tariff letters. Approximately

12–15 letters were expected to be sent on July 7, targeting additional countries

beyond the seven announced (Japan, South Korea, South Africa, Malaysia,

Kazakhstan, Laos, and Myanmar). The full list remains undisclosed.

Counter-Tariff

Warning: Trump’s letters explicitly

warn that if South Africa, Malaysia, Kazakhstan, or any targeted country

retaliates with counter-tariffs on U.S. goods, the U.S. will increase its

tariffs by an equivalent amount. For example, the letters state, “If for any

reason you decide to raise your Tariffs, then, whatever the number you choose

to raise them by, will be added onto the 25% [or respective rate] that we

charge.” This mirrors warnings issued to Japan and South Korea, signaling a

broader policy to deter retaliatory measures.

Additional

10% Tariff Threat: Trump’s July 6,

2025, Truth Social post threatened an additional 10% tariff on BRICS nations

(including South Africa) and their partners (like Malaysia and Kazakhstan) for

supporting “anti-American policies,” such as de-dollarization or alternative

payment systems. This threat was made during the BRICS summit in Rio de

Janeiro, where leaders criticized U.S. tariffs and discussed local currency

trade. South Africa’s 30% tariff and Malaysia and Kazakhstan’s 25% tariffs may

already reflect this punitive approach, given their BRICS affiliation.

Economic

and Geopolitical Implications:

South

Africa: The 30% tariff threatens

its platinum exports, critical for U.S. industries, and could exacerbate

economic challenges in a country reliant on IMF loans. As a BRICS member, South

Africa’s leadership has criticized U.S. tariffs, with Brazilian President Lula

da Silva calling them “irresponsible” at the Rio summit.

Malaysia

and Kazakhstan: Their 25%

tariffs target key exports like semiconductors (Malaysia) and oil/alloys

(Kazakhstan). Their BRICS partner status and Belt and Road (BRI) ties make them

vulnerable to further escalation if they align closer with China or Russia.

Economic

Impact: The U.S. imported $351

billion in goods from the seven countries (including Japan and South Korea) in

2024, with South Africa, Malaysia, and Kazakhstan contributing $35.1 billion.

Higher tariffs could raise U.S. consumer prices, with estimates suggesting a

$1,200 annual cost per household. Markets reacted negatively.

Tariff War

Risks: Retaliation by South

Africa, Malaysia, or Kazakhstan could trigger higher U.S. tariffs; tariffs, escalating trade tensions. Brazil’s

Lula da Silva emphasized the “law of reciprocity,” suggesting BRICS nations may

respond with counter-tariffs, risking a trade war.

The tariffs reflect Trump’s hardline stance against

BRICS and their partners, particularly over de-dollarization concerns. South

Africa’s unchanged 30% rate and Malaysia and Kazakhstan’s lower-than-expected

rates (25% vs. 26% and 27%) suggest selective pressure, possibly tied to BRICS

alignment. The August 1 implementation date aligns with the extended tariff

deadline, but the lack of negotiation progress indicates these rates are likely

final unless last-minute deals emerge. The threat of additional tariffs for

BRICS-related activities could further complicate trade relations, especially

if South Africa or others.

United

Kingdom: A deal maintains a 10% tariff, with

preferential treatment for autos (lowered from 25% to 10% for the first 100,000

vehicles, limited based) but retains 25% sectoral tariffs on steel and

aluminum.

China: A framework agreement reduces tariffs from 145% to

40% (20%+Fentanyl 20%) for 90 days, with China easing export restrictions on

rare earths; the US has eased chip design software; Negotiations continue for a

broader deal

Trump’s

Make in America thrust at the Tariff gunpoint.

On July 7, Trump posted letters on Truth Social to

seven countries, including BRICS member South Africa (30% tariff), BRICS

partners Malaysia and Kazakhstan (25% each), and non-BRICS China savvy nations,

Laos and Myanmar (40% each), Japan, and South Korea (25% each). These tariffs,

effective August 1, include a clause increasing U.S. tariffs to match any

counter-tariffs imposed by these countries. Trump also encouraged almost all

the nations exporting consumer goods to the US, but now facing higher tariffs

to manufacture goods in the US without any tariffs. Trump also promised all

help and quick services including speedy regulatory approvals for setting

factories/production facilities in the US.

Responses from

BRICS and EU:

·

Brazil:

President Lula da Silva called Trump’s 10% tariff threat “a big mistake” and

“irresponsible” on July 7, hinting at reciprocal counter-tariffs. Brazil, with

a $7.2 billion trade surplus, likely benefits from the August 1 deadline extension,

as it has not received a tariff letter.

·

China: The

Chinese Foreign Ministry condemned Trump’s tariffs as “coercion and pressure,”

stating, “there are no winners in a trade war.” China’s temporary 10% tariff

framework (down from 145%) may extend to August 1, but its yuan-based trade

push risks further tariffs.

·

EU: European

Commission President Ursula von der Leyen, on July 7, stressed that Europe

“must show strength” and “unity” in U.S. trade talks, following a “good

exchange” with Trump. The EU, facing a potential 50% tariff, seeks exemptions

for key sectors and likely benefits from the August 1 extension.

August 1

Deadline Extension:

On July 7, White House Press Secretary Karoline

Leavitt announced that Trump would sign an executive order extending the July 9

deadline to August 1 for countries negotiating in “good faith” (e.g., EU,

India, Canada, Brazil, and China). Vietnam’s deal secures its 20% tariff, while

South Africa, Malaysia, and Kazakhstan face fixed 25–30% tariffs due to stalled

talks. Additional letters expected on July 8 may target other BRICS members/countries.

Economic

and Geopolitical Implications:

·

Vietnam: The 20%

tariff, though lower than 46%, could reduce Vietnam’s GDP growth by 1.2% (from

8% to 5% in 2025), impacting industries like footwear (25% of Nike’s U.S.

supply) and electronics. The 40% transshipment tariff pressures Vietnam to

tighten controls on Chinese goods, straining its balancing act with China, a

key investor and neighbor.

·

BRICS: South Africa’s 30% tariff and Malaysia

and Kazakhstan’s 25% tariffs target their $35.1 billion combined U.S. trade

surplus, reflecting Trump’s focus on BRICS’ de-dollarization. China and

Brazil’s pushback risks escalating trade tensions if counter-tariffs are imposed.

·

EU and Global

Trade: The EU’s $209 billion trade surplus and Vietnam’s $123 billion surplus

highlight their stakes in avoiding high tariffs. A trade war could cost the

U.S. $432 billion in GDP and raise consumer prices by $1,200 per household

annually.

·

De-Dollarization:

Trump’s tariffs aim to deter BRICS’ local currency initiatives, but China’s Xi

Jinping, visiting Vietnam soon, may leverage anti-U.S. sentiment to deepen

economic ties, potentially accelerating de-dollarization.

Legal

Uncertainty: The U.S. Court

of International Trade’s ruling against Trump’s use of the International

Emergency Economic Powers Act (IEEPA) for tariffs, under a Federal Circuit stay

until a July 31 appeal, creates uncertainty for all tariffs, including

Vietnam’s.

Outlook: If

new Trump tariffs are implemented at all from August 1, 2025

·

Vietnam’s trade

deal mitigates the 46% tariff threat, but the 20% rate and 40% transshipment

penalty will raise U.S. consumer prices and challenge Vietnam’s export-driven

economy. Its BRICS partner status keeps it vulnerable to the 10% tariff threat

if de-dollarization efforts intensify.

·

South Africa,

Malaysia, and Kazakhstan face higher tariffs (25–30%) without extensions, while

Brazil, China, and the EU leverage the August 1 deadline for better terms. New

tariff letters on July 8 may escalate pressure on other BRICS members.

·

Trump’s strategy

uses tariffs to counter BRICS’ influence and protect U.S. workers, as Leavitt

noted, but unified responses from China, Brazil, and the EU, plus Vietnam’s

delicate China-U.S. balance, risk a broader trade conflict.

Economic Challenges:

The tariffs have raised concerns about economic

impacts, with estimates suggesting an average tax increase of $1,200 per U.S.

household in 2025 and a potential 0.9% GDP reduction if fully implemented with

retaliatory measures.

Legal

challenges add uncertainty: The

U.S. Court of International Trade ruled Trump’s use of the International

Emergency Economic Powers Act (IEEPA) for “fentanyl” and reciprocal tariffs

unconstitutional, but a stay by the Federal Circuit keeps tariffs in place

pending a July 31 appeal hearing.

President

Trump has escalated his tariff threats against BRICS nations (Brazil, Russia, India, China, South Africa,

Egypt, Ethiopia, Indonesia, Iran, and the UAE) and countries aligning with

their policies, particularly in response to their discussions on reducing

reliance on the U.S. dollar (USD). On July 6, 2025, Trump announced via Truth

Social that any country aligning with the “anti-American policies” of BRICS

will face an additional 10% tariff, with “no exceptions.” This threat was made

during a BRICS summit in Rio de Janeiro, where leaders criticized U.S. tariff

policies for disrupting global trade and supply chains. Overall, BRICS nations

are also worried about the recent US pattern of using the USD as a weapon in

scoring geopolitical issues.

The term “anti-American policies” was not

explicitly defined but likely refers to BRICS’ efforts to promote trade in

local currencies, explore alternative payment systems, replace US-controlled

SWIFT, or reform global financial institutions like the IMF, which challenge

U.S. economic dominance. Various BRICS countries are also exploring the idea of

a common currency (using the Gold standard) and common trade like in the

EU/EUR. Trump has repeatedly threatened a 100% tariff on BRICS nations if they

create a new currency or back any alternative to replace the U.S. dollar as the

global reserve currency. This threat, first issued on November 30, 2024, was

reiterated on January 30 and February 13, 2025.

Trump said: “We require a commitment from these Countries that

they will neither create a new BRICS Currency, nor back any other Currency to

replace the mighty U.S. Dollar or, they will face 100% Tariffs, and should expect

to say goodbye to selling into the wonderful U.S. Economy.”

The threat targets BRICS’ discussions on

de-dollarization, spurred by U.S. sanctions on Russia and Iran, which have

pushed members to explore alternatives like the Chinese Yuan or a potential BRICS

payment system to bypass SWIFT. At the July 6–7, 2025, BRICS summit in Rio de

Janeiro, leaders issued a joint statement expressing “serious concerns” about

unilateral tariffs, implicitly criticizing Trump’s policies. They also backed

initiatives to enhance cross-border payments in local currencies and supported

a BRICS Multilateral Guarantees initiative to lower financing costs.

Brazil, the current BRICS president, and other

members like Russia and China have downplayed plans for a common currency, focusing

instead on reducing dollar dependency through local currency trade. Russia’s

Dmitry Peskov stated in January 2025 that talks on a BRICS currency “are not

taking place now,” emphasizing joint investments instead. The BRICS tariff

threats are part of Trump’s broader trade strategy, with the July 9 deadline

marking the end of a 90-day pause on steep tariffs announced on April 2, 2025.

As of July 7, Trump confirmed that letters detailing country-specific tariff

rates (10% to 70%) are being sent to dozens of countries, including BRICS

members, starting July 7, effective August 1 unless deals are reached.

BRICS countries like India and China are

negotiating trade deals to avoid higher tariffs. India is close to a “mini

trade deal” with a 10% average tariff, while China has a temporary framework

reducing tariffs from 145% to 10% for 90 days. These negotiations may be

complicated by the additional 10% tariff threat for BRICS-aligned policies.

Treasury Secretary Scott Bessent indicated

flexibility, noting that countries negotiating in “good faith” could see

extensions beyond July 9, potentially to August 1 or Labor Day. However,

Trump’s hardline stance suggests limited willingness to extend deadlines for

BRICS nations perceived as challenging U.S. interests.

Trump’s threats could backfire, accelerating

de-dollarization by pushing BRICS nations toward alternatives like the yuan or

gold. The U.S. dollar’s dominance (58% of global foreign exchange reserves)

remains secure in the near term, but coercive tariffs may weaken its long-term

role.

China’s Foreign Ministry opposed using tariffs as

“a tool to coerce others,” signaling potential retaliation. Other BRICS

members, like India, advocate that diplomacy to clarify those diversifying

trade mechanisms is not anti-American but a move toward multipolarity. South Africa and Brazil have publicly stated that no

plans exist for a BRICS currency, focusing instead on local currency trade.

India’s Prime Minister Narendra Modi, has cautioned against BRICS appearing as

a replacement for global institutions, indicating a cautious approach. Russia,

minimally affected due to low U.S. exports since the 2022 Ukraine war,

continues to push for alternative payment systems, while China promotes the

yuan and digital currencies like e-CNY.

The additional 10% tariff threat adds uncertainty

to ongoing trade talks as the July 9 deadline looms. While some BRICS nations

like India and China may secure temporary deals, others face higher tariffs

from August 1. The 100% tariff threat remains conditional on de-dollarization

moves, which BRICS leaders currently downplay. Trump’s strategy appears to

combine negotiation leverage with punitive measures to maintain U.S. economic

dominance, but risks escalating trade wars and alienating key partners. The

legal challenge to his use of the International Emergency Economic Powers Act

(IEEPA), pending a July 31 appeal, could further complicate tariff

implementation.

Ongoing/stalled

Trump Tariff Negotiations:

·

European Union: The EU has agreed to a 10% tariff on many exports but seeks exemptions

for pharmaceuticals, alcohol, semiconductors, and aircraft. Talks are ongoing,

with a 25%-50% tariff looming if no deal is reached by July 9; the US may have

offered the EU a 10% tariff deal with caveats. The EU could secure baseline tariff exemptions for aircraft and spirits

in a US trade deal. The EU is exploring a potential deal on cars to offset US

car exports against imports.

·

India:

Indian officials extended their stay in Washington to negotiate, seeking an exemption

from a 26% tariff. The U.S. pushes for market access in agriculture, dairy, and

energy, but India resists, particularly on genetically modified crops. A deal

is not yet finalized, but a mini deal may happen; India may also get 10%

minimum tariffs in exchange for almost 0% tariffs on US goods and limited

access to US farm products into the Country.

·

Canada:

Trade talks resumed after Canada scrapped a digital services tax following

Trump's threat to end negotiations. A deal is targeted for July 9

·

Other Countries: About 100 smaller nations are expected to face a 10% tariff, with

little negotiation progress. Countries like Lesotho, Cambodia, and Madagascar

face higher tariffs (up to 50%) due to limited negotiating power.

On April 2, 2025, Trump imposed steep reciprocal

tariffs (up to 50%) on nearly all trading partners, dubbing it "Liberation

Day" after decades of perceived trade abuse by almost all US trading

partners. A week later, after both Wall Street and Main Street panicked, Trump

announced a 90-day reciprocal tariff pause till July 9, reducing most tariffs

to a 10% baseline to allow negotiations for bilateral trade deals. This pause

expires on July 9, 2025, after which country-specific tariffs could revert to

higher rates (10% to 70%) unless deals are reached or the deadline is extended.

Now, Trump is again extending the tariff deadline to August 1, 2025.

Earlier, Trump had signaled he may not extend the July 9

deadline, stating in a Fox News interview that letters will be sent to

countries (starting July 4 or 5) specifying tariff rates effective August 1,

ranging from 10% to 70%. He emphasized a hardline approach, saying, “I don’t

think I’ll need to [extend],” though he added, “I could, no big deal. However,

White House officials, including Treasury Secretary Bessent and Press Secretary

Karoline Leavitt, have suggested flexibility. Bessent predicted a “flurry” of

deals before July 9 and indicated that countries negotiating in “good faith”

might see extensions, potentially until Labor Day. Leavitt noted the deadline

is “not critical” for such nation.

Trump has acknowledged the complexity of

negotiating with over 170 countries, shifting toward sending letters to set

tariff rates rather than pursuing detailed bilateral deals for all. He plans to

notify 10–12 countries daily starting around July 4, with rates based on how

they “treat” the U.S. The administration’s approach appears to blend

negotiation with unilateral tariff impositions, maintaining pressure on trading

partners but risking economic uncertainty and retaliatory tariffs.

Trump’s

Truths and media bytes:

·

I am pleased to

announce that the UNITED STATES TARIFF Letters, and/or Deals, with various

Countries from around the World, will be delivered starting at noon (Eastern),

Monday, July 7th. Thank you for your attention to this matter! DONALD J. TRUMP,

President of The United States of America.

·

Any Country

aligning themselves with the anti-American policies of BRICS will be charged an

ADDITIONAL 10% Tariff. There will be no exceptions to this policy. Thank you

for your attention to this matter!

Conclusions

Trump kept around 20-25% tariff rates for most of

the countries, while close allies/trading partners like the EU may get 10% and

permanent adversary countries like China may get 40% (including 20% Fentanyl

tariffs). The potential weighted average tariff rate after Trump’s latest

tariffs, effective August 1, 2025, and various sectoral tariffs (25%-50%) may

be around 22.5%; China alone constitutes around 15% of total US merchandise

imports. This is slightly lower than the 27.5% weighted average tariffs announced

on April 2, Liberation Day and in line with 19.5% FROM April’25 (Trump 2.0).

But it’s still significantly higher than 2.5% weighted average rates till

January’25 (pre-Trump 2.0).

Trump extended his new tariffs rhetoric to the August

1 deadline by which various affected countries may have an opportunity to offer

a better deal to the US for getting lower tariffs. Although Trump should not

further extend his tariff deadline as it may keep the Fed on the sidelines till

December’25, considering the looming festival season (X-Mas), various US

retailers and importers may have already placed orders to big exporters like

China, Vietnam etc. Thus, Trump may not distort the supply chain further till

at least September’25 or even December’25.

So, if Trump does not get a better deal, he may

again extend the tariff deadline to September or even December’25. Although

Trump always maintains that exporters like China pay his tariffs, not US

importers, it’s laughable. Tariffs are import duties to be paid by importers

when foreign goods enter the US. Higher tariffs are usually borne by importers

and consumers. But in this case, as the US is the world’s biggest consumer

(departmental stores), exporters may have to sacrifice some margin either from

their own pockets or to be compensated partly by their respective government

(export subsidies).

The Fed is assuming Trump tariffs may be borne

equally by exporters, importers, and US consumers at 1/3rd each. But

Trump’s weighted average tariffs at present rates may be around 22.5%, which

would be much higher than the Fed’s best-case scenario of 15.5% and closer to the

base case scenario of 25.5%. Overall, Fed’s uncertainty may remain at around

22.5% weighted average tariffs vs 2.5% prior, the cost of living may be higher

if exporters and importers do not absorb at least 70% of the higher tariffs. If

they attempt to retain market share, their margin (EBITDA) will be affected to

some extent; if not the US economy may head towards a stagflation-like scenario

due to subdued discretionary consumer spending.

Bottom line

Trump’s higher tariffs around 222.5% may cause both

subdued consumer spending and corporate report card, both of which are negative

for Main Street as well as Wall Street.

Market

impact

Wall Street gained almost 0.8% on Thursday, July 3,

on Trump’s tax cut/BBB bill optimism, easing of tariff war tensions and fading

concern of a hard landing after the expected NFP/BLS job report for June’25.

Techs helped on easing of tech war tensions after the Trump administration

withdrew export restrictions on chip-design software to China. Chip-design

stocks like Cadence Design and Synopsys surged, while Datadog soared after its

imminent inclusion in the S&P 500. While a few mini trade deals have been

secured, the goal of “90 deals in 90 days” has not materialized, with only

three mini agreements finalized.

After the long weekend holiday, Wall Street Futures

stumbled Monday, July 7, on escalated Trump trade war tensions as Trump imposed

higher-than-expected tariffs on various countries. Trump imposed a 25% tariff

on imported goods from South Korea and Japan, slated to start from August 1. USD surged, while Gold slipped.

At the same time, Trump imposed additional levies

on 12 other countries, with tariff rates ranging from 25% to 40%. Countries

affected include South Africa (30%), Indonesia (32%), Thailand (36%), Malaysia

(25%), Myanmar (40%), Laos (40%), and Kazakhstan (25%). Bangladesh and Serbia

will face a 35% tariff. These measures are set to take effect from August 1,

2025.

On early Tuesday, July 8, Wall Street Futures were

almost flat, while Gold slipped further after a report that the US has proposed

a deal to the EU that would retain a 10% baseline tariff, with exceptions for

sensitive sectors such as aircraft and spirits. The market got some relief in

the extended timeline for negotiations, as the new tariffs are not set to take

effect until August 1st, allowing more time to reach agreements.

Technical

outlook: DJ-30, NQ-100, SPX-500 and Gold

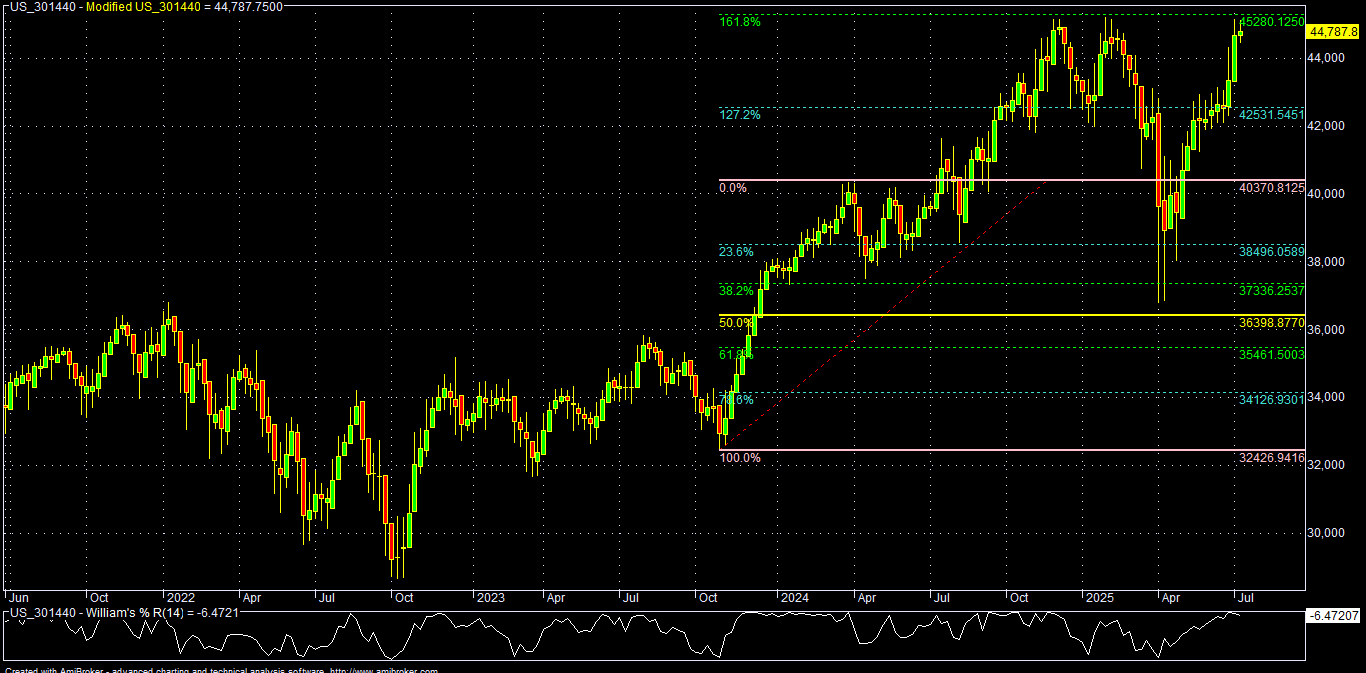

Looking

ahead, whatever may be the narrative, technically Dow Future (CMP: 44800) now has to sustain over 45000 for a

further rally towards 45300/45800* and only sustaining above 45800, may further

rally to 46100/46500-47100/47200 in the coming days; otherwise sustaining below

44950, DJ-30 may again fall to 44200/43900-43400/42400 and

41700/41200-40700/39900 in the coming days.

Similarly,

NQ-100 Future (23000) now has

to sustain over 23100 for a further rally to 23200/23600-23800/24000 and

24100/24450-24700/25000 in the coming days; otherwise, sustaining below 22900,

NQ-100 may again fall to 2400/22200-21900/20900-20700/20200 and

19890/18300-17400/16400in the coming days.

Looking

ahead, whatever may be the fundamental narrative, technically SPX-500 (CMP: 6275) now has to sustain over 6400-6450 for

a further rally to 6525/7000-7500/8300 in the coming days; otherwise,

sustaining below 6350/6300-6250/6200, SPX-500may again fall to

6000/5800-5600/5300 in the coming days.

Technically

Gold (CMP: 3350) has to sustain over 3375-3395 for a

further rally to 3405/3425*-3450/3505*, and even 3525/3555 in the coming days;

otherwise sustaining below 3365-3360, Gold may again fall to 3340/3320-3300*/3280

and 3255/3225-3200/3165* and further to

3130/3115*-3075/3015-2990/2975-2960*/2900* and 2800/2750 in the coming days.